In 2019, the Current Health Expenditure (CHE) in the Philippines rose to Php792.6 billion, based on the Philippine Statistics Authority (PSA). In addition, CHE is the total amount spent by the government, HMO providers, insurance companies, and out-of-pocket (OOP) shouldered by Filipinos for health care.

And 47.9% of which is from the individual pockets of Filipinos.

As a result, a huge health insurance gap to address, as it pushes approximately 1.5 million Filipinos into poverty each year. Consequently, it forces families to cut back on education and vital spending.

Hence, insurance companies must work harder to fill this gap. On the other hand, we have seen improvements in out-of-pocket expenditure from 56.3% in 2017. It translates to a slight improvement in the overall health care in the country.

Table of Contents

Health Insurance Gap

Undeniably, the pandemic shocked the world, especially the medical industry. However, challenges in health care are an existing problem in the country. In other words, the COVID-19 pandemic amplified the situation.

Many Filipinos died because they cannot access the medical treatment they needed.

While some survive only to face poverty, there’s a great need for life and health insurance which plays a vital role in nation-building.

The Rising Cost of Getting Sick in the Philippines

In 2017, there were about 4 Million Filipinos who had HMO coverage. In spite of that, the average maximum benefit limit (MBL) is only Php150,000.

It is small, but still a big help to ailing employees.

However, it is not enough to cover major medical health concerns such as stroke, cancer, heart attack, etc.

It gives a false security blanket that is enough. Because a stroke costs around Php 1.8 million which is way beyond the average MBL. In addition, a heart attack costs Php 900,000, breast cancer at Php 430,000, and lung cancer at Php 2.7 million.

Meanwhile, the difference between the MBL and the actual cost of treatment is what we call the “out-of-pocket.”

You have two choices when you get ill.

Firstly, cover the medical cost by selling your properties or using your savings intended for other things, such as the education fund for your kids, building a house, starting a business, etc.

Secondly, transfer the risk to an insurance company by getting life and health insurance.

How do we come up with the list?

Many companies are claiming the number 1 spot as the top life insurer. Moreover, some blogs and websites have decided to consolidate the data from the Insurance Commission (IC). But the question is, “Is it the correct way of digesting the data?”

So don’t worry this blog is here to help you with the confusion.

In April 2022, IC released five (5) financial reports, and different companies topped each metric. But among the five (5) categories, only one is widely used to come up with the top 10 life insurance companies in 2022. It is not just in the Philippines but the entire world and that’s “Premium Income.”

Premium Income is the revenue that an insurer receives as premiums paid by its customers for insurance products. When a customer purchases an insurance product, such as a health insurance policy, the customer’s cost for a specified term of the insurance policy is called the premium. (Investopedia)

How to interpret the categories

The other metrics are also important. For instance, you use it to assess the overall financial health of a company.

You may interpret the categories in this way.

Premium Income

It is the combination of the past and present business of the insurance company.

The past business is often called the renewal premiums. And a good percentage of renewals means that clients are happy with the services, so they continue paying for their plans. Furthermore, it means that the company’s business is of quality.

In addition, the present business is what we call the NBAPE.

New Business Annual Equivalent (NBAPE)

It signifies the sales performance of an insurance company in a given year. Therefore, it is vital to acquire new business. That is to say that the new business annual equivalent reflects how the general public perceives a company.

Thus, growth is desirable, while a decline means losing interest or trust.

Net Income

It is equal to the income minus expenses. Thus, it shows how profitable the business is. Importantly, you will be placing your hard-earned money through insurance, so you must consider profitability.

Of course, you want the company to be there when the time comes.

Net worth

It is equal to the assets minus liabilities. Undeniably, it shows the capacity of a company to cover liabilities, such as claims.

Use this to foresee if the company can cover future claims.

Total Asset

It is composed of current and fixed assets. Likewise, here you can see how the company manages its assets. Thus, a good company should have growing assets to support the business and sales.

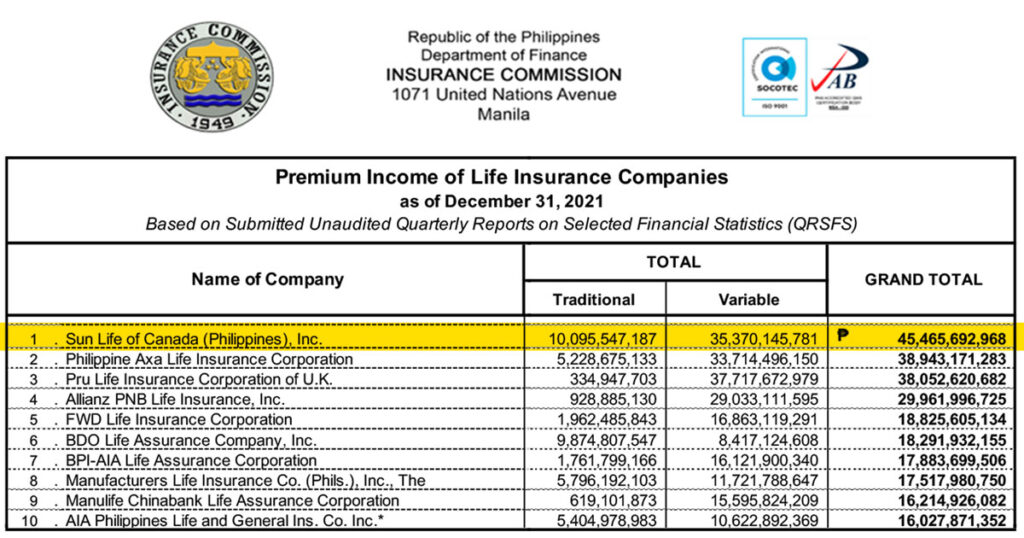

Sun Life Remains the Top Life Insurance Company in 2022

Sun Life is the number one insurer of 2022 based on the latest performance released by the Insurance Commission last April 2022. Thus, It is the 11th consecutive time that Sun Life managed to top the premium income category both in traditional (whole life, term, and endowment) and variable plans.

So why is being the number one (or being part of the top 10) crucial to you as an insurance buyer?

Because it serves as a validation that companies like Sun Life can still fulfill their promise to their clients.

Remember, life insurance is an aleatory or a promise contract, that when a specified event occurs like death, the insurer will have to pay the promised amount.

Of course, you want your family to get the benefits by the time it happens to you, right?

Sun Life’s Traditional and VUL Plans

It’s essential to consider the standing of an insurance company before availing of any insurance plan. You want that by the time the need arises, the company is still performing well to fulfill its obligations to you. But this shouldn’t be your sole basis for getting a plan. Undoubtedly, you might as well consider convenience, customer service, a reputable Financial Advisor, etc.

A VUL plan is perfect if you want income protection with a wealth accumulation plan. It lets you grow your money while giving you financial security and peace of mind. So click the link below to request a quotation and financial consultation.

READ: Sun Maxilink Prime | Best-Selling VUL Plan of Sun Life

Health is wealth. So get the most comprehensive health insurance in the country covering 114 critical illnesses. Make sure you get the treatment you need when you need it most. So click the link below to learn more.

READ: Sun Fit and Well | Most Comprehensive Health Insurance Plan

*****

Top 10 Life Insurance Companies in the Philippines 2022

Now, let us know more about the other companies that complete the list. As mentioned before, we based the top 10 life insurance companies in the Philippines in 2022 on premium income. The table below summarizes the overall performance of each company.

| Insurance Company | Premium Income | NBAPE | Net Income | Net Worth | Total Assets |

|---|---|---|---|---|---|

| Sun Life | 1 | 2 | 2 | 3 | 1 |

| AXA | 2 | 3 | 5 | 7 | 3 |

| Pru Life UK | 3 | 1 | 8 | 10 | 5 |

| Allianz PNB Life | 4 | 4 | 13 | 19 | 9 |

| FWD | 5 | 6 | 10 | 11 | 12 |

| BDO Life | 6 | 5 | 7 | 5 | 8 |

| BPI-AIA | 7 | 7 | 6 | 6 | 7 |

| Manulife | 8 | 8 | 4 | 4 | 6 |

| Manulife Chinabank | 9 | 9 | 24 | 16 | 10 |

| AIA Philippines | 10 | 10 | 1 | 1 | 2 |

So here are the top 10 life insurance companies in the Philippines in 2022.

1. Sun Life of Canada (Philippines) Inc.

Officially founded in 1895, Sun Life of Canada (Philippines) is the first and oldest life insurance company in the Philippines. Undeniably, the ability to fulfill its promises to its clients has made Sun Life the preferred life insurance company in most households. No wonder it is still the top life insurance company in the country.

READ: Sun Life | A Company that Loves to Pay Claims

➡ Premium Income: 1

➡ NBAPE: 2

⬇ Net Income: 2

⬇ Net Worth: 3

⬆ Total Assets: 1

Sun Life remained the number 1 life insurance company in the Philippines in 2022 for 11 consecutive years based on Premium Income.

In addition, in terms of NBAPE, it’s only a place behind Prulife with a modest margin of Php 75 Million.

However, there is a slight decline in net worth and net income, while it overtakes AIA Philippines in Total Assets snatching the number 1 spot.

READ: Sun Maxilink Prime | Best-Selling VUL Plan of Sun Life

2. Philippine AXA Life Insurance, Corp.

AXA Philippines was only established in 1999 in the Philippines but has shown massive growth and market penetration thanks to its bancassurance business. Another key point, it is a joint venture between AXA Group and Metrobank Group.

➡ Premium Income: 2

➡ NBAPE: 3

➡ Net Income: 5

⬇ Net Worth: 7

➡ Total Assets: 3

Indeed, the company is stable and has maintained most of its placement in all categories except for Net Worth, which declined by one place. Despite being a stable company, it almost didn’t grow in acquiring new business.

3. Pru Life Insurance Corp. of UK.

The company started in 1996, 23 years in the life insurance industry in the Philippines. Despite being relatively new compared to its rivals, Pru Life UK bagged 3rd place in the list.

➡ Premium Income: 3

➡ NBAPE: 1

⬇ Net Income: 8

⬇ Net Worth: 10

➡ Total Assets: 5

Furthermore, Pru Life maintained its Premium Income, NBAPE, and Total Assets position. Despite retaining the number one spot in NBAPE for two years, there was only very little difference in its performance from Sun Life. There was also a noticeable decline in its net income by four (4) places and net worth by three (3).

4. Allianz PNB Life Insurance, Inc.

Allianz PNB Life was founded in 2001, operating as a subsidiary of Alliance SE. The company is in 4th place in the top 10 life insurance companies in the Philippines, a massive leap from 10th place last year.

⬆ Premium Income: 4

⬆ NBAPE: 4

➡ Net Income: 13

⬆ Net Worth: 19

➡ Total Assets: 9

Truly, Allianz PNB’s business is a game-changer this year. It made considerable advances in premium income by advancing three (3) places, four (4) in NBAPE, and seven (7) in net worth, while there are no changes in its net income and total assets.

5. FWD Life Insurance Corporation

In 2014, FWD started in the Philippines. Despite being a relatively new player in the industry, they manage to be in the top 10 life insurance companies in the Philippines in 2022.

⬆ Premium Income: 5

⬇ NBAPE: 6

⬆ Net Income: 10

⬆ Net Worth: 11

➡ Total Assets: 12

FWD advances five (5) places in terms of premium income, while its NBAPE declined by one (1). They also showed improvement in net income and net worth, while no changes in their placement in total assets.

6. BDO Life Assurance Co. Inc.

Founded in 1999 as a joint venture between Generali Pilipinas Holdings Company Inc. (GPHC) and BDO. But now, BDO Life Assurance Co. Inc is the new name of Generali.

⬆ Premium Income: 6

⬆ NBAPE: 5

⬆ Net Income: 7

⬆ Net Worth: 5

➡ Total Assets: 8

Additionally, BDO Life has now coped with the pandemic as they advance by two (2) places in terms of premium income and NBAPE. Then the company moves from 30th place to 7th place in terms of its net income. Lastly, net worth increased by three (3).

7. BPI-AIA Life Assurance Corportation

Previously known as Ayala Life Assurance Incorporated, founded in 1933. It is the country’s top bancassurance on the list thanks to the strategic alliance between BPI and Philam Life.

⬇ Premium Income: 7

⬇ NBAPE: 7

⬆ Net Income: 6

⬇ Net Worth: 6

➡ Total Assets: 7

BPI-AIA slides by two (2) places in premium income and NBAPE. The net income declined while it maintained 7th place in total assets.

8. Manulife Philippines

Manufacturers Life Ins. Co. (Phils.) or just Manulife is a wholly-owned subsidiary of The Manufacturers Life Insurance Company. It was then established in 1907, making it one of the oldest insurance companies in the Philippines.

⬇ Premium Income: 8

⬇ NBAPE: 8

⬇ Net Income: 4

➡ Net Worth: 4

➡ Total Assets: 6

Premium income and NBAPE slide by two (2) places. Its net income also declines, while there’s no movement in its placement in net worth and total assets.

9. Manulife Chinabank Life Assurance Corporation

The company is a strategic alliance between Manulife Philippines and China Bank. It aims to provide a wide range of innovative insurance products and services to China Bank customers.

⬆ Premium Income: 9

⬆ NBAPE: 9

⬇ Net Income: 24

⬇ Net Worth: 16

⬆ Total Assets: 10

In addition, Manulife Chinabank advanced by two (2) places in terms of premium income and to the top 10 life insurance companies in the Philippines.

Their last appearance on the list was in 2019.

The NBAPE increased by four (4) places. Despite the increase in renewals and new business, the company faced a significant decline in net income and net worth. On the other hand, there’s a little increase in their total assets.

10. AIA Philippines

AIA Philippines, formerly Philam Life, was founded in 1947 by Cornelius Vander Starr and partner Earl Carrol. Undoubtedly, their incredible partnership made Philam Life the number 1 life insurance company in 2 years, 1949, in the business.

⬇ Premium Income: 10

⬇ NBAPE: 10

⬆ Net Income: 1

➡ Net Worth: 1

⬇ Total Assets: 2

Additionally, there is a tremendous drop for AIA Philippines in Premium Income by 6 in just a year. There’s also a decline in NBAPE by one (1) while it maintained its spot in net worth. The company also lost its number 1 spot in terms of total assets, which it held for several years, to Sun Life.

Top 10 Life Insurance Companies in the Philippines (NBAPE) 2022

Getting more clients means generating more income for business expansion and payment of claims. It can also lower administrative and insurance charges, thus, more allocation in the investment fund of your VUL plan or dividends for a traditional insurance plan.

Pru Life UK dominated this category with Php 8.83 billion worth of new business premiums. However, Sun Life comes in 2nd with a small margin at Php 8.56 billion.

You may refer to the table below for a more comprehensive look at the performance of each life insurance company in 2022.

| Insurance Company | NBAPE |

|---|---|

| Pru Life Insurance Corp. of U.K. | P8,832,276,212 |

| Sun Life of Canada (Philippines), Inc. | P8,756,709,868 |

| Philippine AXA Life Insurance. Corp | P5,299,332,475 |

| Allianz PNB Life Insurance, Inc. | P5,299,332,475 |

| BDO Life Assurance Company, Inc. | P3,401,015,642 |

| FWD Life Insurance Corp. | P3,401,015,642 |

| BPI-AIA Philippines Assurance Corporation | P2,523,937,081 |

| Manufacturers Life Ins. Co. (Phils.), Inc., The | P2,375,186,979 |

| Manulife Chinabank Life Assurance Corporation | P1,938,131,214 |

| AIA Philippines Life and Generali Ins. Co. Inc. | P1,708,113,235 |

Top 10 Life Insurance Companies in the Philippines Based on Net Income 2022

In a nutshell, net income is the total profit of a company after subtracting all the expenses in operating a business. Accordingly, AIA Philippines has reclaimed the top spot from Sun Life this year.

| Insurance Company | Net Income |

|---|---|

| AIA Philippines American Life and General Ins. Co., Inc. | P12,989,797,150 |

| Sun Life of Canada (Philippines), Inc | P8,386,484,311 |

| Insular Life Assce. Co., Ltd., | P4,671,018,878 |

| The Manufacturers Life Ins. Co. (Phils.), Inc., | P3,481,434,346 |

| Philippine AXA Life Insurance. Corp | P2,750,907,186 |

| BPI-AIA Philippines Life Assurance Corporation | P1,997,980,539 |

| BDO Life Assurance Company Inc. | P1,994,401,913 |

| The Pru Life Insurance Corp. of U.K. | P1,527,327,215 |

| Sun Life GREPA Financial, Inc. | P597,705,861 |

| FWD Life Insurance Corporation | P493,892,209 |

Top 10 Life Insurance Companies in the Philippines Based on Net Worth 2022

Philam Life remained the number 1 spot in the net worth category or the amount by which the assets exceeded their liabilities, followed by Insular Life, Sun Life, and Manulife.

| Insurance Company | Net Worth |

|---|---|

| AIA Philippines American Life and General Ins. Co., Inc. | P71,179,150,021 |

| Insular Life Assce. Co., Ltd., The | P43,921,758,564 |

| Sun Life of Canada (Philippines), Inc | P32,704,787,938 |

| Manufacturers Life Ins. Co. (Phils.), Inc., The | P13,387,114,017 |

| BDO Life Assurance Company Inc. | P10,544,707,624 |

| BPI-AIA Life Assurance Corporation | P8,178,514,579 |

| Philippine AXA Life Insurance. Corp | P8,171,999,666 |

| Sun Life GREPA Financial, Inc. BDO Life Assurance Company, Inc. | P4,645,804,897 |

| United Coconut Planters Life Assce. Corp | P4,489,364,419 |

| Pru Life Insurance Corp. of U.K. | P3,500,325,002 |

Top 10 Life Insurance Companies in the Philippines Based on Assets 2022

An asset is anything expected to bring future benefits by generating cash flow, reducing expenses, increasing sales, etc. After several years, Sun Life has overtaken AIA Philippines in total assets.

| Insurance Company | Total Asset |

|---|---|

| Sun Life of Canada (Philippines), Inc. | P282,776,856,737 |

| AIA Philippines American Life and General Ins. Co., Inc. | P276,307,876,721 |

| Philippine AXA Life Insurance. Corp | P164,817,651,848 |

| Insular Life Assce. Co., Ltd., The | P151,020,392,175 |

| Pru Life Insurance Corp. of U.K. | P125,026,023,889 |

| Manufacturers Life Ins. Co. (Phils.), Inc., The | P118,851,740,232 |

| BPI-AIA Life Assurance Corporation | P115,662,867,791 |

| BDO Life Assurance Company, Inc. | P81,054,673,167 |

| Allianz PNB Life Insurance, Inc. | P78,416,721,162 |

| Manulife Chinabank Life Assurance Corporation | P56,787,192,136 |

RELATED: Sun Maxilink Prime | Best-Selling VUL Plan of Sun Life

How to Pick the Right Life Insurance?

Looking for the right insurance plan as a first-time insurance buyer is such a daunting task. Don’t worry. It is okay.

Everyone started somewhere. And after getting your first insurance choosing the succeeding plans are much easier.

But for now, you may follow the steps below to find the “right” plan.

5 Steps in Getting the Right Insurance Plan

1. Choose 5 insurance companies

Firstly, determine what qualities you are looking for, like positive customer service, financial standing, and competitive pricing, and narrow your choices by picking three (3) to five (5) companies from the top 10.

But be careful here because when we say price, the cheapest isn’t always the best insurance.

So look at the value first before its price.

2. Know what’s important for you

Let me ask you, “What are your top 5 priorities.” Before getting those proposals, you must understand yourself first. So don’t be like one who just got an insurance plan without a goal.

It is your family whom you want to protect from financial struggles.

Or nowadays, the rapidly increasing cost of medical care is a concern.

Maybe you want to secure your kids’ future by providing the best education and a roof over their heads.

Likewise, some people think about retirement or what to do as a retiree. Perhaps open a business to keep you busy?

So make sure to reflect on how important this decision is for you. But again, I’ll tell you that getting insurance is a long-term commitment.

Problems will shake you from time to time. Consequently, you might surrender the plan without a clear purpose of why you started. Of course, I know you don’t want to waste your time and money.

Thus, set your goals at this point.

3. Schedule an Appointment

Get in touch with an advisor in each company and set a meeting with them.

It is for your future, so do not just browse the pages of the proposals you get as if you are browsing a menu; you are not in a restaurant.

Life insurance is for your future, so take time to have a sit-down discussion.

Here are some qualities to look for in an advisor.

- He must be reachable. Can you contact your advisor in times of need? An advisor should be around to check your account and do regular policy updates. For instance, there are times when you’ll forget your coverage and may need a refresher on your plan. So refrain from getting an advisor you are intimidated to ask.

- Is he knowledgeable? Can he explain the plans and options well? Also, you might have heard somewhere to read the fine print of an insurance plan. Yes, you need to know the pros and cons of it, but a knowledgeable advisor will always lay it down without reservation. Because he is not just after the sale but genuinely cares for you.

- A dependable person. Remember that you will be getting not just an insurance plan but also a partner. Thus, consider your insurance plan as your contingency plan that concerns your family’s future. Do you think he is still with the insurance company when your need arises?

Choosing the right advisor is as hard as picking the most suitable insurance plan. In addition, an insurance plan is like proof of how much you care for your family. But on the flip side, an advisor is your partner, or let’s say, the caretaker of that proof. So be mindful of considering a reachable, knowledgeable, and dependable advisor.

4. Prepare questions

At this point, you may now prepare for questions that concern you the most. But then you don’t have to compute for each fee/charge every year. Do you have to know the production cost of the bag of chips you buy? I don’t think so.

In step 3, you have set your goals. Price should not be the basis but its value proposition.

Your advisor will answer all your questions during the product presentation.

Thus, ask if you have remaining questions.

Again, this is for your future, so make sure the plan answers your needs.

5. Finalize your decision

Now that you have met the five (5) advisors and reviewed their proposed plan. At this point, you may create a table or list of things you need and want from an insurance plan versus the proposals.

So which among them is the fittest to your goal?

While some riders or benefits are good additions, remove them if it doesn’t fit your cause. Just get what you need accordingly.

I hope this blog helped you get the “right” insurance plan.

Cheers!

READ: Sun Fit and Well | Most Comprehensive Health Insurance

*****

References:

- de Vera, Ben O. (2021, April 20). Insurer profit down 8.6 percent in 2020 as pandemic hammers markets. Inquirer.net. Retrieved May 29, 2021, from https://business.inquirer.net/322053/insurer-profit-down-8-6-percent-in-2020-as-pandemic-hammers-markets

- Funa, Dennis B. (2019, June 19). The health insurance gap in the Philippines. Business Mirror. Retrieved May 29, 2021, from https://businessmirror.com.ph/2019/06/19/the-health-insurance-gap-in-the-philippines/

- Mapa, Dennis S. (2020, October 15). Health Spending Grew by 10.9 Percent in 2019. PSA. Retrieved May 29, 2021, from https://psa.gov.ph/pnha-press-release/node/163258

- Tan, Arlyn. (2021, April 28). [Fin Talk] Life Insurance Company Ranking: What’s in it for the Policyholders and Beneficiaries?. Now You Know. Retrieved May 29, 2021, from https://www.nowyouknowph.com/post/fin-talk-life-insurance-company-ranking-what-s-in-it-for-the-policyholders-and-beneficiaries?

Ton is an electronics engineer, financial blogger, insurance agent, and a certified investment solicitor. A multi-awarded financial advisor with clients ranging from lawyers, doctors, engineers, accountants, business owners, company directors, and OFWs to minimum wage earners had sought advice from him in achieving lifetime financial freedom.